The second half of 2020 has been eventful for the portfolio in very different ways than the first half, so I thought it was time for a quick update on a few positions. Overall I’ve been pretty pleased with YTD performance but, in hindsight, there have been some obvious mistakes that I will probably explore in more detail in a separate post later in the month. For now, here are some updates in chronological order:

Sold Central European Media (CETV) 9/1/20: This was a merger arb position that I wrote a little about in late June. The spread closed quickly once the acquirer (PPF) finally got around to officially filing with the European Commission thus signaling their intent to move forward. In retrospect there was still a little more juice to squeeze here but I’d captured the bulk of the returns and was ready to move on. 24% in < 3 months is fine by me.

Sold Fuling Global (FORK) 9/1/20: This was another “arb” position on a Chinese manufacturer that I never got around to writing up but did tweet about (shameless plug to follow me on Twitter if you don’t already). I say “arb” because it was total speculation on a quick repricing of a management buyout offer. Management (and existing controlling shareholders) lobbed in an offer on 6/22/20 that was a 6% premium that was already optically cheap. The thing was basically already left for dead here in U.S. markets and dirt cheap (assuming it wasn’t an outright fraud) so a take private made a lot of sense. With the acquirer being so deeply involved with day to day operations already, it looked to me like a call option on the board behaving like a real, independent board (possibly a big ask for a Chinese company, but the downside was pretty muted). They ultimately negotiated a slight bump from $2.18/share to $2.35/share and I closed at $2.30 for a 9% return in a little over 2 months (weirdly, I coincidentally opened and closed CETV and FORK on the same day).

Bought Rubicon Technology (RBCN) 10/15/20: write up here

Partial sell of Collector’s Universe (CLCT) 11/3/20: I trimmed my CLCT position at $65/share, which now looks pretty silly given yesterday’s news that the company has been offered $75.25/share in a take private transaction. The trimming had nothing to do with my intermediate/long term view on the firm at the time (or now) and was mostly a risk-control function for the portfolio. CLCT had gotten to >20% weight in the portfolio. In this situation, I was a little uncomfortable with that and am fine taking some chips off the table from time to time, especially when sentiment has shifted so radically in such a short amount of time. Regarding the take private deal by Cohen, Turner, et al., the press release cites a 30% premium to VWAP but that’s a measly 4% premium to close prior to the announcement. A lot of CLCT’s run this year has been driven by renewed interest in the company thanks to Connor/Alta Fox and (I believe) the emerging market view that CLCT was a play on COVID trends (accelerated interest in the collectibles space). I think it’s clear that there is still a ton of value that could be captured moving forward and that $75.25/share is an absolute steal for the private investor group given the untapped potential here. I can’t say that I’m surprised that management is trying to give the company away given their already mediocre track record. I’m not sure what to make of some of the language in the filings but I will be extremely surprised if the deal gets done anywhere near $75.

Bought additional Dream Unlimited (DRUNF) 11/12/20: No real epiphany or antyhing here, I just continue to build confidence in Dream and like what they are doing. I wanted to make it a little larger position, despite buying at prices +20% above my initial purchase, so I added just a little more in the middle of the month.

Sold FitBit (FIT) 11/23/20: I also exited my arb position in FitBit. Like CETV there was a little more profit to be had, but I felt that I’d gotten enough (~13% in 6 months). Also, I’m not sure how much longer this situation drags out given that all of the big regulators seem to be in a Mexican standoff with their global peers waiting for someone to try to stop this deal.

There you have it. All in all it’s been a great few months for the portfolio from both an absolute and relative return perspective. It’s quietly turned into a very nice year for the broader small/micro cap universe as well. Hopefully we can all hang onto these gains through a nice and quiet December.

Rubicon is a left-for-dead net-net in the midst of a multi-year turnaround

The company is trading below the net cash value on the balance sheet and is now under control of several capable allocators

The Numbers:

Price $8.45

Mkt Cap $20M

EV -$5M

Net $/share $10.20

The Company:

Rubicon Technology (RBCN) is a microcap based in Bensenville, Illinois that specializes in the design and production of monocrystalline sapphire products for optical and industrial applications (such as windows, optical systems, and use in semiconductors). Prior to 2016 it also sold its products to LED and mobile device manufacturers, but elected to exit that business as a result of competitive forces. Despite a long and, at times, profitable operating history RBCN fell on hard times beginning in 2012. From then on it has posted only one profitable year (2018), fought off a delisting with a reverse split, and saw the departure of numerous management team and board members – all while struggling to “right-size” its production capacity and refresh its business strategy. Today the company is controlled by a cadre of smart allocators that are pivoting the business and monetizing assets, all while trading for well below the value of cash on the balance sheet.

The Good:

This is usually the section of the write-up where I talk about the juicy margins, the interesting business model, or some hidden growth potential. There’s none of that here. It’s pretty clear to me that the future of RBCN looks radically different than it’s past and does not involve sapphire production. Since 2016/2017, several notable activists have established significant positions in RBCN and begun the turnaround process. Their progress has taken awhile to unfold, but has included: replacing the previous management team & board, monetizing underutilized assets and protecting NOLs, as well as one small acquisition. Before we get too far, let’s run through the folks involved:

Timothy Brog (3% of shares) is the current CEO of RBCN and the MD of Locksmith Capital. I don’t know much about Mr. Brog or Locksmith but some quick Googling tells me he has turnaround/deep value experience and at least one good outcome (Peerless Systems PRLS) in the recent past.

Jeff Gramm/Bandera Partners (11% of shares) is on the board. Full disclosure I’m a big fan of Jeff’s and if you haven’t read his book Dear Chairman on shareholder activism already, I highly recommend it.

Sententia Partners (6% of shares), most recently of Schmitt/Ample Hills Twitter fame, are also involved.

Aldebaran Partners (6% of shares) is also listed as a major shareholder. Don’t know much about them, but Google tells me they are a Graham-style value outfit out of Indianapolis

Over the course of the last few years RBCN has shuttered a lagging business line and monetized a number of real estate (and other) assets under current leadership. I’ve not been able to find much in the way of commentary from management or those involved but ti’s pretty clear to me that the incentives are aligned here. Check out the disclosures on compensation incentives for Mr. Brog as outlined in the most recent DEF14 filing:

“In 2019, Mr. Brog was eligible to earn up to 40,500 shares (the “2019 Objective Bonus Shares”) of the Company’s common stock if certain goals were achieved. While Mr. Brog’s 2018 goal for earning his bonus was based solely on preserving and building capital through liquidation of assets, management of short-term investments, and reductions of liabilities, his 2019 goals included several specific, and more qualitative, targets that the Board believes are critical to the long term success of the Company. There is no set formula to weight the importance of each target — the Board will consider Mr. Brog’s performance in relation to all three targets when determining the amount of his bonus.

Goal 1: Progress towards an acquisition

The Board wishes to incentivize Mr. Brog to further develop the Company’s acquisition pipeline, with the ultimate goal of finding suitable acquisition targets and eventually closing a transaction. To achieve Goal 1, the Board wants to see material progress from Mr. Brog in improving deal-flow and allocating more time to the search for acquisitions. A signed purchase agreement or the actual consummation of an acquisition would also satisfy Goal 1.

Goal 2: Signed purchase agreements for the Malaysia properties

The Board believes the Company’s assets in Malaysia continue to be an unwanted distraction from Rubicon’s domestic operations. Mr. Brog would achieve Goal 2 by negotiating and signing a purchase agreement for one or both of the Malaysia properties with Board approval. Material progress in finding a buyer for the properties will also be considered by the Board for achieving Goal 2.

Goal 3: 2019 Year-End Cash

Similar to in 2018, the Board wishes to incentivize Mr. Brog in his efforts to preserve capital.”

Even if Mr. Brog hadn’t accomplished these goals (he did), this still signals to me that everyone involved is on the same page and rowing in the same direction. Notice also that goal number one is pretty relevant to the future trajectory of the company. RBCN announced in May of 2019 that it had acquired the assets of a Indianapolis pharmacy and launched “Direct Dose RX” which will be “focused on the delivery of prescription medication, over-the-counter drugs and vitamins to skilled nursing facilities and hospitals for patients that are being discharged” with licenses to operate in 11 states. I can’t seem to find a purchase price disclosed anywhere and based on the revenues that RBCN has begun showing in the financials the progress has been minimal, but I think this is a signal about how the company plans to move forward – taking interesting shots at new business lines completely outside the realm of their current/historical industry.

The Bad:

Probably the biggest question in my mind with RBCN is why bother continuing the old sapphire business at all. They exited the LED/mobile device business in 2016 but the remaining line sounds very similar. The space sounds competitive, they have high customer concentration, there’s commodity pricing elements to the business that make costs hard to predict, there’s high capital intensity, etc. My thought would be to shut it all down entirely and start fresh with your cash pile. Although I can’t find it mentioned in the filings, the only guess I can make is that they are locked into some supply contracts that would be prohibitively expensive to break and therefore have to see them through. Whatever the case, personally, I wouldn’t mind seeing the sapphire business go away entirely.

To play devils advocate, one might also question the Direct Dose RX acquisition in general. It looks to be relatively small ($300k in revenue over first 6 months of 2020) and unprofitable at the moment, plus I assume it will consume some capital to get it up and running. In the end, one could wonder how meaningful this could even be to the financial results. However, my opinion is that it’s probably just too early to tell on this one and at the end of the day you have to trust the judgement of the management team and board.

In a lot of ways, owning RBCN is a “bet on the jockey” situation. You’re hoping that these activists can come together and generate some value for shareholders, and there’s a lot of potential here. They’ve got $25M in cash plus some other assets and NOLs to work with, a pretty low burn rate on the existing business (about $2-$3M/yr in losses as far as I can tell), and a rock bottom valuation (which they have been taking advantage of by buying back shares). It’s a real turnaround story, but I like the odds of something good happening.

Key Variables to Monitor:

Continued monetization of legacy assets – they recently completed the sale of some Malaysian real estate and have a number of other real estate assets to divest.

Cash conservation/burn rate – moving forward I’ll be keeping a close eye on cash levels and the profitability/costs of the legacy business which could all impede further progress on the turnaround

Progress on acquisition(s) – obviously the big catalyst here is the completion of an acquisition of some sort which might prove to be challenging in this environment given the dry powder in the hands of private equity firms and SPAC management teams right now.

Conclusion:

In my writeups I typically try to give some estimate of upside and downside but net-nets are a weird corner of the market where the valuations are already illogically low, so I’ll punt on the valuation part this time around. But suffice to say I have a hard time seeing the valuation get much lower than this and I see a ton of upside potential given the opportunity for a quick shift in the narrative around the company. Take for example the aforementioned Schmitt Industries (SMIT) which has appreciated ~50% since announcing their acquisition of Ample Hills Creamery in July. While not a perfect comparison, I think that shows how quickly things can change with these “left-for-dead” microcaps.

I hope that I’ve made the investment case obvious for RBCN, but obviously DYODD. This falls into my “special situations” bucket in the portfolio and I’ve put it in at ~3% position but am looking to add on any pullbacks.

Gravity is one of the names in the portfolio that I haven’t officially written up here on the blog, but has really carried the portfolio (along with CLCT) over the last few months. I haven’t taken the time to do a full write up on it because I personally would not be comfortable initiating a new position anywhere near the current prices, so I didn’t feel that there was much value in it for readers. GRVY is up about 260% YTD and +300% from my initial purchase a little over a year ago, so maybe it would have been more valuable to write it up than I thought. Nonetheless, this post is not meant to be a victory lap in any way. Instead, I want to use Gravity as an example of a concept I’ve been thinking a lot about lately: hidden value, specifically franchise value. I don’t mean “franchise value” like the way people think about Apple (i.e. brand), but “franchise value” as in valuable (and in this case undervalued) intellectual property.

Gravity is a South Korean small cap game developer/publisher with a focus on mobile games. Their primary asset is a 20 year old piece of IP called Ragnarok, which has taken many forms over the years but whose most popular incarnation has been as a fantasy-based MMORPG whose primary player-base is focused in southeast Asian markets.

EDIT: It should be noted that Gravity does not, in fact, own the Ragnarok IP outright, but instead have a licensing agreement with the content creator. According to their 2019 20F filing this agreement ends January of 2033. While this fact is pertinent to the long term investment case for GRVY, I felt it was beyond the scope of this post. As always, do your own due diligence. (h/t @gamesinvest)

Promotional art for one of Gravity’s most popular properties Ragnarok OnlineGameplay screencap from Gravity’s Ragnarok M: Eternal Love

At the time of my initial purchase GRVY was trading at <3x trailing EV/EBITDA and <5x trailing P/E. At first glance, it was undeniably cheap but for a laundry list of valid reasons:

It’s a small cap – even now with the run up in price its market cap is sub-$1B

Despite it’s NASDAQ listing, it’s headquarters is based in Seoul, South Korea and primarily operates in SEA markets – all things that I suspect to be deterrents for American investors

It’s a controlled company – Japanese game developer GungHo Online owns ~60% of GRVY shares

From it’s NASDAQ IPO in 2005 to 2016, the stock was down ~95%, rendering it effectively dead to most investors

The company has failed to pivot away from the success of the Ragnarok franchise into any other successful properties of note

With their 2018 annual filing, the company disclosed material weaknesses in their accounting controls and introduced remedies to address the situation

From a personal perspective, I find the gaming (especially mobile-based) industry generally unattractive. My perception is that game development is expensive, predicting the success of any given game is extremely difficult, and the entire industry is subject to whiplash-inducing fluctuations in consumer tastes. I think GRVY financials are evidence of this – quarterly revenues, profits, etc. are extremely variably from quarter to quater due to sporadic launches of new titles and staggered roll outs across geographic markets.

Despite all of this, I thought I recognized something interesting about Gravity. Growing up, I was intimately familiar with a similar franchise that perhaps you have heard of: Pokemon. Although you may not realize it, Pokemon is widely reported as the highest grossing media franchise of all time. While I am in no way implying that Gravity’s Ragnarok property could approach anything close to Pokemon’s value, I do think there are some similarities to the business mechanics. Specifically, the content strategy is pretty simple: every few years you refresh the property with some new content/characters/storylines and release a whole slew of new products (in Gravity’s case new games/expansions). The only limits to the amount of marginal content is your imagination, beyond that you need only to make the economics of additional products work. I was encourage by the simple fact that Gravity had survived as a growing concern for nearly two decades on this IP alone – clearly there was some longevity to the property, some “franchise value.”

When you think about it, the strategy is pretty obvious. Once you have some demonstrated success with a property, you reheat that content and serve it up in as many varieties as possible. Pokemon’s catalog of content, for instance, includes trading cards, comics, cartoons, movies, video games, licensed merchandise, etc. Gravity’s Ragnarok is still limited just to video games, but the principle remains the same – there is always room for expansions, add-ons, bonus content, geographic-specific content, and so on. But all of that only works if you have a nostalgia-fueled base of loyal fans, which I would propose that a 20 year track record validates. Beyond that you must also consider the upside optionality of finding traction with a new generation of fans. Every release, every expansion, every launch in a new geographic market is an opportunity to bolster that base and create new devotees. Of course, the holy grail is that someday Gravity/GungHo set their sights somewhere outside of the realm of video games and start leveraging the content in other media formats.

The problem here is that franchise value like this isn’t captured on any balance sheet – it requires some abstraction from the financials. I found the Pokemon comparison to be useful, but the fact is that there are any number of other franchises with similar mechanics (sports franchises like Madden, FIFA, etc.; Harry Potter; college textbook content is notoriously rehashed over and over with monopolistic economics). The real key here is finding it in a publicly traded entity and at a sufficiently cheap price.

When I bought GRVY, I categorized it into the deep value/mean reversion portion of the portfolio (read more about my thinking on that here). With these holdings, my thesis is basically that the market has priced a company irrationally cheaply and that you don’t need many good things to happen in order to reverse that, regardless of the long-term quality of the business. I thought it was clear that GRVY could generate impressive returns on capital, but that they were quite lumpy. However, there would be a lot of opportunity for the market to reconsider it’s assessment of GRVY as they are constantly launching new titles in new markets and creating opportunities for success. Plus, at the time, it had about a third of its market cap in cash and no debt on the balance sheet. It was a classic example of what I usually look for: high upside optionality (if a new game is a smash hit) and limited downside (as a result of their strong financial position).My point here is that the siuation didn’t require some complex insight, deep understanding of industry dynamics, or intense scuttlebutt. At sufficiently cheap valuations you just need something to go right.

[I would, at this point, be remiss if I did not mention the work of a few Swedish investors from whom I have gained considerable insight on GRVY just by following their Twitter feeds. They do far higher quality work and more granular analysis than I could hope to do. If you’re at all interested in GRVY check out: @ValueGARP, @Pappakeno1 and @89OlleEdit: See also @lilsneakyfox and @pokertrader1 (h/t @ValueGARP)]

Anyway, this was quite a ramble but I wanted to get some thoughts out there about GRVY because I think it is/was an interesting situation. Again, just to reiterate, I would not be looking to open a position at current prices but I do think the characteristics here are quite informative when evaluating future media properties. I hope you got something out of this. Thanks for reading.

A piece of news that caught my attention awhile back was the announcement that Aaron’s (AAN) intends to split its two primary business lines into stand alone publicly traded entities. I’m always game for a nice corporate action catalyst in small/mid-cap land and I have kept my eye on competitor Rent-A-Center (RCII) for some time now (without having actually gotten around to taking a deep look). For the uninitiated, Aaron’s is a U.S. based NYSE listed mid cap ($3.5B) that describes itself as a provider of lease-purchase solutions to underserved and credit-challenged customers. Basically, if you are someone with dicey financial history and living paycheck-to-paycheck but would like to purchase furniture, appliances, electronics, jewelry, etc. Aaron’s will sell you these items on a payment plan. You get the items you want with little to no upfront payment, but pay some interest above standard purchase price to compensate them for the credit extension.

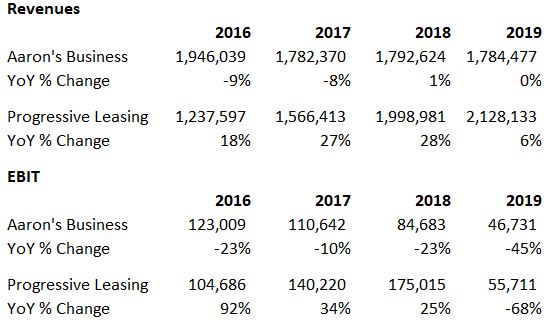

Over the years, the business has diverged into two distinct segments: the store-level operations (which will retain the legacy Aaron’s branding moving forward) and the leasing/financing business (to become standalone “Progressive Leasing” post-separation). On the surface, the split is kind of a no brainer. The legacy Aaron’s business has a number of obvious headwinds: 1,400 brick and mortar locations in an increasingly online world, low margins & sluggish growth, and intense competition from existing competitors (Rent-A-Center) and new entrants (Big Lots). Meanwhile, Progressive has gradually overtaken the legacy Aaron’s operations to become the primary business line. At this point it’s essentially a consumer financing franchise focused on the underwriting and extension of credit to subprime borrowers – it just so happens to be attached to the legacy Aaron’s brand. Progressive has been growing by establishing partnerships with retailers like Best Buy, Ashley Furniture, Cricket Wireless, Lowe’s, etc. to provide their underwriting and financing services to their own customer bases. In sharp contrast to the dwindling albatross it’s currently handcuffed to, Progressive is actually growing and offers better seemingly better economics. The numbers below tell the story pretty effectively.

You might notice the screeching halt in revenue and EBIT growth for Progressive in 2019. For revenues, an accounting change forced them to start netting some allowances for doubtful leases against top line revenue whereas they previously reported those costs in bad debt expense (so in previous years imagine revenues are 5-7% lower than reported in this table). As for EBIT, turns out Progressive got in a little trouble with the FTC and paid a $175M penalty to settle the inquiry in 2019. So, excluding the penalty, they were on track for more growth.

At this point my thinking is that there are a couple of angles to play here:

Go with the logic of the logic of the corporate action – Progressive is clearly the better business. You could:

Buy AAN now, wait for the spin and sell the Aaron’s stock on spin date

Wait until the spin date and buy the Progressive stock outright hoping to be early before the market notices that it’s a much better business

Wait for the Greenblatt special:

Wait for the Aaron’s stock to be sold to an illogically cheap level post-spin and scoop it up for a bargain once the selling has subsided

See if the Progressive business trades cheaply (post-spin it will still be in the low mid-cap/high small-cap range so maybe it gets ignored altogether) and try to pick it up post-spin without having to touch Aaron’s

So the logical next step is to look at valuations on these two and see if there’s some potential value here.

Aaron’s

I’ll start with this because I think it’s very straightforward. Aaron’s easiest comp is clearly Rent-A-Center (RCII) which operates a very similar business model (including having a financing component similar to Progressive) and trades pretty reliably around 10x TTM earnings. If I apply that multiple to a “normalized” earnings estimate for 2020 assuming no growth/shrinkage from 2019 figures, I get to about $700M in market value. FYI I still think there’s all sorts of problems with this estimate – they are constantly taking write downs and restructuring charges, earnings have been declining anywhere from mid single digits to high teens YoY for awhile now, and I think 10x may be a little optimistic given that RCII has a leasing component with (presumably) better economics than a pure play Aaron’s will. But, sure, $700M in estimated value.

Progressive

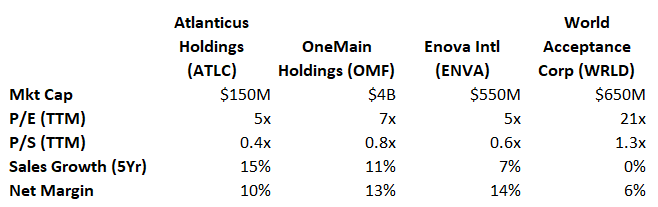

I’ll admit that I’m not very familiar with this type of financial services business. I have no doubt that it’s a better business than Aaron’s but I was a little surprised that the economics weren’t better than the <10% EBIT margins that show up in the reporting. Plus, I suspect that it is pretty cyclical given that you are dealing with uncreditworthy borrowers to begin with. Nonetheless, the attraction here is clearly the potential for continued growth. So in trying to value this thing I tried to find some comps that did something remotely similar in the consumer/retail subprime finance space to see what sort of valuations were out there. Here’s what I found:

The only real outlier appears to be WRLD, which seems to trades a premium to others for some reason that I can’t quite discern based on a quick look at the financials. Either way the cohort is not very encouraging. Assuming you get 25% EBIT growth (2020E EBIT = $280M, less 21% statutory tax rate = E of $220M) and applying a seemingly optimistic 10x P/E multiple, I only get to $2.2B in market value. At 1x sales and assuming 20% revenue growth for 2020, you could get to $2.5B.

So, together I am saying that Progressive ($2.5B) and legacy Aaron’s ($700M) should be worth about $3.2B. AAN’s current market cap is $3.7B. Whoops! Clearly something is awry here.

If I’m AAN management, I’m not doing this transaction for kicks and giggles. I’m doing it because I think one of two things:

There’s actual value to unlock here – Progressive is much more valuable than the market is giving credit for and should trade at more of a premium as a standalone. I think in this case you are banking on a multiple higher than 10x earnings post-separation, in which case my valuation above is not high enough. Objectively, if all you showed me was an anonymous company with revenues growing at +20% over a handful of years with positive earnings I’d say it probably trades over 15x earnings. That would put Progressive somewhere in the +$3B market cap by itself.

The legacy Aaron’s business is so bad and dying so quickly that I need to throw it overboard to save Progressive before it’s too late. This implies that Progressive is more or less fairly valued but that the Aaron’s business is worth much less than the $700M I estimated above.

To be honest, I can’t tell which it is (and maybe it’s some of both).

I think the wild card is the valuation on Progressive. There’s definitely a goodco/badco dynamic here and it’s tough to determine just how much legacy Aaron’s is weighing on Progressive. To be fair this was a very quick and dirty look and I could be completely missing a ton of nuance here, but I don’t think that it’s obvious that there’s going to be a lot of value unlocked here. You would really need an outlier multiple assessment on Progressive to see a meaningful move up, which isn’t to say that won’t be the case – I’m sure AAN has spent a ton of money on bankers and consultants that have told them this is a slam dunk. So that is certainly within the realm of possibility given that the growth has been very strong and there appears to be a long runway (there are lots of potential retailers that could be customers). But I don’t know that I would want to hang my hat on a rich valuation as my base case and, to be honest, having looked at both sides of the business now I don’t find either particularly attractive irrespective of the corporate action.

I will of course watch this fairly closely, but I think the verdict here is a pass for me. I hope this was at least somewhat informative for you and if you have a different perspective on the situation I’d love to hear from you. Thanks for reading.

I don’t normally write up names that I don’t invest in, but I spent so much time on this one that it felt like a waste not to get some blog content out of it. Plus, I want to memorialize my thoughts on StoneX (SNEX) here and now so that when it’s (inevitably) a multi-bagger in a few years I can point to this post and call myself a moron for not putting money into it.

Let me start by saying that I REALLY wanted to pull the trigger on SNEX. It has a number of the attractive qualities that I like in a portfolio company: an interesting rollup/platform build strategy, a focused management team, a niche industry, clear room for growth, generally misunderstood by the market, etc. I just couldn’t quite get all the way comfortable with it, but it’s definitely going to be high on my watch list and I could easily see talking myself into it a position later on.

It’s funny – I actually spent a little time back in 2018 or 2019 looking at SNEX (then still INTL) but didn’t get very deep before I felt it was too complicated and moved on to simpler things. My ears perked up after I heard Jeremy Raper (@puppyeh1) on Special Situations Cast discussing the company’s impending acquisition of GAIN Capital (GCAP) and what a steal it looked to be. I put it on my to-do list and didn’t think much more about it. A few weeks ago Jeremy made an appearance on the new Yet Another Value Podcast with Andrew Walker (@AndrewRangeley) and talked more about the company (now officially post-deal and re-branding) and at that point I thought there was enough to warrant further work. I spent a ton of time looking at this thing and trying really hard to talk myself into it, but here we are so let me lay it out as I see it.

StoneX, formerly known as INTL FCStone (INTL), is a U.S.-based small cap financial services company serving retail, institutional, and enterprise customers around the world in a variety of products/services. SNEX pitches themselves as a rollup of various niche financial services, which rings true when you take a look at their business lines, which include: commercial hedging/consulting, securities (lending & market-making), physical commodities trading, global clearing & execution services, and global payments processing. The current management team has been in place since 2003 and has built the company as a platform in which they are looking to add new offerings or bolster existing business lines via acquisitions. These are usually money-losing/breakeven bolt-ons of smaller sub-scale businesses at attractive acquisition prices where synergies with the existing platform offer a path to future profitability. Historical results have been impressive over the past 15 years or so as the company has grown book value at around a 20% CAGR. Incrementally, growth is a little lumpy given the volatile nature of revenues/income, but over a long enough time frame you can see the value grinding higher.

High level, here are some things I really like about the business:

As of the beginning of 2020 SNEX has begun their re-brand to StoneX from the legacy INTL FCStone branding and completed, as far as I am aware, their largest acquisition to date (Gain Capital – GCAP) which appears to be a homerun of a deal (they claim a purchase price of 4x next year fully-synergized EBITDA). They have also just crossed over the $1B market cap (although they also did this briefly in mid-2018) which might garner more attention from investors. I think this confluence of factors offer a great opportunity for the market to ‘reset’ the narrative on the company and reassess SNEX’s value .

Their general roll-up strategy makes a lot of sense to me. They buy (usually) unprofitable, small businesses that offer access to new services/clients and can be quickly restructured into the existing SNEX platform as profitable contributors. This deepens their service offerings for existing clients and creates cross-sell opportunities for the acquired client base. Reading through the rationale on the Gain transaction really crystallized the value/rationale on the acquisitions for me – it’s clear that there are meaningful economics that can be wrung from these businesses (at least in GCAP’s case) and that management is intensely focused on the execution and how it impacts shareholder value.

They operate in niche business lines. Their core business began as a consultancy and trading execution service to commodity users (i.e. commodity producers or consumers). In addition to that business they now have a variety of complimentary offerings from high-margin global payments processing to low margin securities lending and everything in between. Logically, putting all of these things together makes sense to me because it adds a lot of value to client relationships while creating certain economies of scale/synergies across the platform.

From a portfolio composition perspective, SNEX thrives when markets are at their most volatile. High volatility in their service markets (equity, fixed income, commodities, etc.) means more trading, wider spreads, etc. which all lead to higher revenues and profitability for the firm. Theoretically, if equity markets are choppy and the rest of your portfolio holdings are struggling, SNEX will be at it’s most profitable.

Here are my main concerns with SNEX:

Although the rollup strategy makes sense to me in theory, I’m not sure that you can be certain about the quality of the acquisitions. GCAP appears to be a killer deal on the surface, but you have little to no visibility to any of the other (albeit much smaller) acquisitions as they get integrated into their respective business lines. In a vacuum, maybe that’s not a problem but SNEX’s business lines have pretty volatile revenue streams which means it’s hard to look at the results, even in aggregate, and draw any meaningful conclusions. I suppose the counter argument here is that over a long enough period of time the ‘average’ economics/results should drive the value realization but I’m having trouble getting comfortable with that.

Since 2003, the stock has achieved ~20% CAGR for shareholders, but a lot of that value was realized in the first 2-3 years when current management took over – the CAGR since 2005 is ~13%. I have a personal problem here which is that I underwrite everything in the portfolio to a 15% hurdle rate. Admittedly that’s a completely self-constructed issue and I’m sure that doesn’t matter to you at all. But it means that I have to look at SNEX and try to figure out what’s different about the next 3, 5, 10, 15, etc. years that’s going get it to a 15%/yr return. Maybe their rate of acquisitions increases meaningfully, maybe we have an extended period of market volatility and the business is suddenly gushing cash – I don’t know but it’s hard for me to pick out something I expect to be meaningfully different with any level of certainty. My ultimate point here is that if you can’t reliably predict any meaningful increases in the bottom line, I think you need a multiple re-rating to get to my 15% hurdle. So speaking of multiple expansion…

Ignoring the nit-picky hurdle rate problem and thinking about it more generally, SNEX looks pretty cheap right now – Koyfin shows a 10x TTM P/E – but that’s coming off two of the best quarters in company history thanks to unprecedented market volatility. Their pro-formas from the GCAP transaction presentation suggest there’s opportunity to add to the bottom line assuming a meaningful amount of cost cutting and synergies, but even by their own estimates that suggests that at today’s prices they’d be trading at 10x adjusted net income two years out. The current prices are also 13x 2019 earnings, which is in the ballpark of their historical average multiple. At the end of the day I think the market has to look at this company and completely re-assess the value. My worry is that the re-rate never happens and, in the meantime, the general cash flow volatility and possibility of underachievement on this rather large acquisition are all on the table. The bear argument here is, and will continue to be, that SNEX is an unfocused amalgamation of related but very different businesses with pretty volatile economics – all characteristics that don’t normally manifest in high multiples. I think the splashy acquisition and the re-brand create an opportunity for the market to take another look but I’m not sure that the story is obvious enough to warrant a meaningful change in pricing.

My last (and sort of obvious) point is that there’s a financial ‘black box’ element to SNEX. They do market making, trading, etc. which means they have some principal capital at risk each and every day, not to mention the implicit liability associated with doing billions of dollars worth of financial transactions on behalf of clients. For instance net income in 2017 was basically $0 because of a huge credit loss on a piece of their physical trading business (although subsequent recoveries have offset almost all of it at this point, to be fair). They are implicated in lawsuits whenever a shady customer implodes and takes a bunch of client money down the drain. I guess my point here is that on any given quarter/year they could step on a landmine and make already volatile earnings even less predictable with a big loss in one of the operating groups.

I spent a lot of time thinking about this situation and ultimately (for now, anyway) decided I couldn’t get all the way committed to the position. Could I be kicking myself, even just a year from now, because SNEX has ripped – absolutely. I could totally see the rebranding and GCAP deal catalyzing a revaluation on the back of some fat TTM financials thanks to 2020’s volatility. It feels like I’m disqualifying SNEX on a personal technicality, but my hurdle is also a key part of my investment process so to cheat and ignore it now just because I really like the narrative/management/whatever feels disingenuous. And maybe there’s something to be said for not pulling the trigger if I’m not fully confident in a position – I think it’s better not to go into a position with shaky hands to begin with. This post was a little ramble-y but I feel like it helped me clarify my soup of thoughts and I hope it was somewhat informative for you. Thanks for reading.

It has been awhile since I wrote up a book review, so I thought I would remedy that by discussing Fortunes in Special Situations in the Stock Market by Maurece Schiller. If you’ve read the rest of the blog, you might recall that I generally consider my “special situations” portion of the portfolio to be my weakest area of ‘expertise’ and to help with that I’ve been trying to read up on the space. I can’t remember exactly how I happened upon Fortunes, but I do recall it being highly recommended and well reviewed. I must admit that I had no familiarity with Maurece Schiller prior to reading the book, but as it turns out it was well worth the gamble. To cut right to the chase, I will say that I absolutely loved the book. In one of the introductory sections one of the books’ contributors, Tom Jacobs of Huckleberry Capital Management, describes Schiller’s works as the Rosetta Stone for special situation investing. While I cannot attest to the quality of the other books (Schiller apparently wrote 4 other titles with similar subject matter), I can whole heartedly endorse Jacobs’ statement. To the extent that one can systematize (or even merely catalog) the process of running a special situations portfolio, Schiller does it masterfully. I highly recommend the book regardless of your familiarity with the special situations investing – I think there’s something here for newcomers and veterans alike.

To contextualize everything for you, the book was originally published in 1961, so some concepts are a little dated. The version I picked up is the 2017 “authorized edition” with includes additional (modernized) interjections & case studies from a group of interested parties (some professional portfolio managers and private investors who are breathing new life into Schiller’s body of work).

The book definitely shows it’s age in some respects; there is ample discussion of railroad and utility breakups/reorganizations that are not particularly relevant to the modern investor, but I think the editors do a nice job of counterbalancing this with modern case studies and commentary. There’s also little to no discussion about activism in the book – I suspect primarily because this is a more modern phenomenon that became more prevalent after the junk bond/corporate raider era in the 80s. Hard to blame Schiller for not having a crystal ball, but I would love a modernized version of the book that examined some newer types of special situations.

As for Maurece Schiller himself, he was born in 1901 on Long Island and attended Dartmouth before making his way to Wall Street as a runner (and eventually broker) in 1922. Schiller spent the rest of his career shuffling between brokerage firms before publishing his own works and opening his own shop. It seems that despite the high quality of his work and the monumental task of systematizing an entire field of the investment industry, Schiller has gone largely unrecognized for his contributions. In the book, the editors boldly describe Schiller’s books as the missing link between The Intelligent Investor (1949) and You Can Be a Stock Market Genius (1997) – which I endorse fully after finishing this book. You can read more about Schiller and the ongoing campaign to bring his works to light at http://maureceschiller.com/

One more thing on Schiller as a person before we get into details – Schiller’s passion for special situations and investing really shines through in his writing. I particularly liked this passage early on in the book:

“While the procedure for making money requires work, it should not be a chore. The very nature of these situations is a stimulating one: in their elements there is the surprise of a windfall, there is unusual romance, like the little bistro in the “off the usual” neighborhood, and there is the stimulation that comes from satisfactorily solving a problem.”

It’s not often you find investors (especially those who write about investing) which such colorful imagery and the guile to use the word “romance” when talking about their work.

Defining Characteristics of Special Situations

I found Schiller’s general descriptions of special situations to be informative and grounding for me. I think a lot of times we, as individual investors, have a jumble of concepts and thoughts in our heads with no real organization or structure. So it’s particularly useful when someone comes along and articulates it as clearly and thoroughly as Schiller.

Schiller begins outlining the concept with this statement:

“Special situations are investments in stocks or bonds that reflect corporate action, meaning activities occurring within the administrative scope of the corporation rather than at the business level. “

It’s a nuanced distinction, but an important one. One of the things I find most appealing about special situation holdings, and ultimately why I choose to incorporate them into my portfolio, is the idiosyncratic exposure that they offer. Schiller goes on to put some finer points on this concept by writing:

“risks are at a minimum and achievement of the expected profit is a calculated probability, regardless of the trend of the securities market.”

“corporate action is an administrative move affecting the capital structure; it is not directly concerned with long term trends of profits or losses from operations of the business”

These are also important supporting concepts because, again, I think these are really the crux of special situations – reduced correlations to broader markets and, as a result, an opportunity for information and/or risk arbitrage.

To that end, the editors included a small excerpt from Ben Graham in Security Analysis that I thought aligned nicely with Schiller’s comments:

“Special situations are the happy hunting grounds for the simon-pure analyst who prefers to deal with the future in terms of specific, measurable developments rather than general anticipations.”

Schillers goes on to further flesh out his definition with these accompanying characteristics:

“Apart from corporate action, which is the common denominator of all special situations, we can usually find the following identifying characteristics:

Profits develop independently of the trend of the securities market.

Risks are at a minimum (reflecting prior knowledge of anticipated profit).

Corporate action is in the development stage.

The securities (stocks, bonds) are undervalued.

Information is available inviting comprehensive analysis.”

The Framework for Special Situations Investing

Schiller sorts the special situations universe into two broad categories: “something doing” companies and “discount situations.”

“Something doing” situations include turnarounds, old companies entering new business lines, large cash asset companies, and what Schiller describes as “new era” companies. Schiller points out, astutely, that the presence of dynamic management teams if often needed in these positions. He also mentions that these types of situations often allow for greater appreciation (i.e. have a higher ceiling) than the “discount” situation category.

One point of contention here: while I agree wholeheartedly with the first 3 items in the preceding list of “something doing” situations, I think the inclusion of “new era” companies shows the age of the text here. Schiller includes industries such as electronics, semiconductors, data-processing, etc. and goes on to discuss the analysis process. These were basically just up-and-coming industries at the time the book was written which strikes me as more aligned with modern “growth” investing rather than true “special situation” investing. I don’t think these fit well into his definition of a special situation and I suspect if Schiller were alive and updating/re-writing the book today he might exclude the “new era” companies from the book entirely.

“Discount” situations are the classic opportunities that we most commonly associate with the value/special situations world: mergers/acquisitions, tenders, spin-offs, recapitalizations/reorganizations, etc. Schiller notes that these situations engender a more methodical approach as there are clear catalysts, timelines, and expected profits/losses relative to “something doing” situations.

Ultimately, the common denominator between the two categories is the corporate catalyst, but equally as important is the ever-present value perspective of the investor.

The Details

Beyond the broad strokes that I have outlined above, Schiller provides a very thorough examination of each type of situation and provides a full blown procedure for analysis and execution. He discusses nearly every aspect of each type of situation – from potential risks to consider and specific sources of information to entry and exit trading strategies and everything in between. I don’t mean to gloss over this aspect of the book, but this is ultimately the heart of the subject, so it would be a disservice to examine these in any greater detail in this brief blog post. Suffice to say that I think it is well worth your time to pick up a copy and read it yourself.

Reading Fortunes has truly opened my eyes to Maurece Schiller’s legacy and the tragic injustice that he is not mentioned among the forefathers of investing. I found it to be extremely informative and a very easy read. I hope that if anything in this post has sparked your interest, you will check out this or any of Schiller’s other works.

Before we get started, I want to (once again) point you to Tyler’s work at Canadian Value Stocks. His writing on Dream formed the basis for my research and got me interested in the name.

The Company:

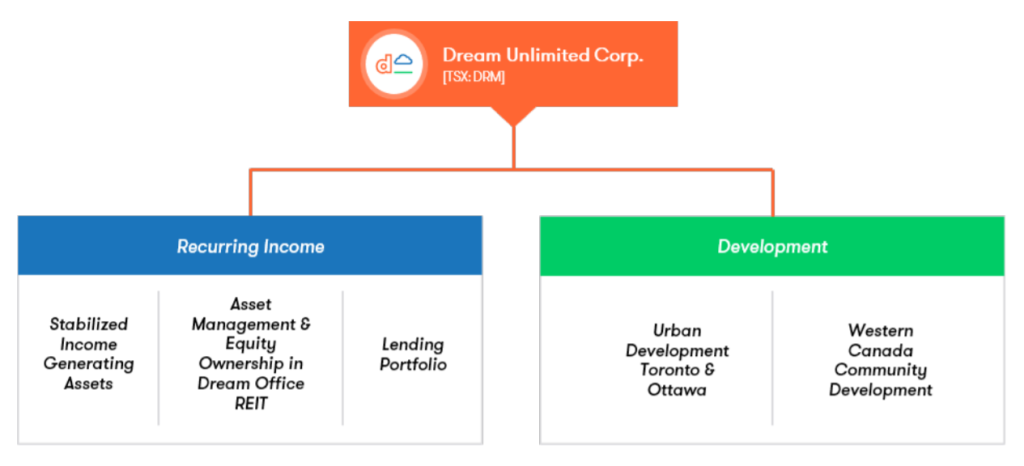

Dream Unlimited (DRM / DRUND) is a Toronto-based real estate development and asset management firm. Dream was founded in 1996 by acting President Michael Cooper, was privatized in 2003 and re-listed in 2013. In that time it has spun out a number of other publicly traded entities – Dream Office REIT (D.UN /DRETF), Dream Industrial REIT (DIR.UN / DREUF), Dream Hard Asset Alternative Trust (DRA.UN), and Dream Global REIT (no longer public as it was acquired by Blackstone in 2019) – which operate within various real estate niches. This write up will focus exclusively on the parent company but it should be noted that the fortunes of all are tied closely together as Dream Unlimited (“Dream” or “DRM” from here on out) is the manager/lead developer for each of the trusts, holds a number of overlapping assets in partnership with the trusts, and (in most cases) is a major direct shareholder of each of the trusts.

Dream splits its business into two primary segments: recurring income assets and development assets. The recurring income segment consists of two underlying lines of business: asset management (fees derived from management of the public REITs and other development agreements plus the ownership stakes in the REITs themselves) and stabilized assets (a variety of income generating properties to be held indefinitely). The development segment is sub-divided into “Urban” (condo, rental, and mixed-use assets in Toronto & Ottawa to be sold or moved to the “recurring income” segment in the future) and “Western Canada” (raw land, housing, commercial, and multi-family assets in Saskatchewan and Alberta that may be sold or held). Assets are split fairly evenly between the recurring and development lines of business.

At this point I would like to say a few things about the rest of my commentary below. I tend to stay away from asset-based valuations, particularly real estate investments. Maybe I’m just dense, but I find real estate to be hard because 1) the accounting is complicated and nuanced and 2) valuations are extremely hard to predict. Call me a dolt, but I like the ease of hanging a multiple on some measure of income/cash flow and calling it a day. So, just a fair warning, take everything you see below with an extra grain of salt. I approached the valuation and research in a way that I thought was reasonable, but I allow for the fact that I am omitting some thing(s) here. I suspect that DRM is more complicated than most given the variety of their assets and business lines. The financials are no walk in the park: they consolidate the Alternatives REIT into their financials (so you have to disentangle all of that), the accounting is different based on the classification of different property types, and it’s hard to normalize anything when there’s constantly fair-value changes and non-recurring transactions happening all the time. Anyway, enough belly aching – I just wanted to up-front with you about the quality of analysis here.

The Good:

I’ll walk through two versions of valuations at the end of this section (a “bear” case and a “reasonable” valuation), but obviously I own it and therefore believe it is cheap by some measure. But before we get there, let’s discuss some easier to digest data points.

First, I believe the company is very well run. Book value per share has grown at about 20% since 2014. Debt to assets stands at about 30%, which appears to be well below peers. Management has communicated (and taken action to implement) a clear emphasis on the quality of income and diversity among the business lines. And, if you’re into owner-operators, you’ll be pleased to know that founder and President of DRM, Michael Cooper, holds 40% of the shares outstanding.

Turning to the business segments themselves, I like the diversity that Dream presents. Although relatively small, I believe the asset management business presents the most interesting opportunity for growth. Dream has the dependable fees from managed REITs, but recently announced a more focused effort on managing outside assets. I believe this is excellent timing given their strong track record with the Dream platform and their recent successful sale of the Global REIT to Blackstone. Within this segment, Dream also holds large positions in the public REITs and opportunistically manages the positions. This creates further cash flows from distributions on the REITs and further magnifies Dream’s exposure to the underlying assets. The stabilized income assets include a mix of residential, rental, commercial, retail, and recreational assets (such as the Arapahoe Basin ski property in Colorado). The profit contributions from this segment are modest but the company has expressed a desire to grow this stream in the future, which should also contribute to more stable cash flows. The development side of the business is where the most tangible potential for appreciation lies, but where uncertainty seems the highest as cash flows/income/etc. are “lumpier”. Dream engages in a range of development projects: residential communities, multifamily housing, hospitality, commercial, office, etc. Often properties are partnerships, either with the public REITs or other third party development partners. Some assets are developed specifically for sale, others will be moved to the recurring income segment once the property is stabilized. From a macro view, I think the business lines provide a unique and somewhat diversified mix of income streams.

Moving on to the valuations below, I will lay out a downside scenario in which I make some fairly draconian assumptions to demonstrate where I think the floor might be, as well as a more reasonable assessment of value assuming a “normalized” environment. In both cases I use as a basis for valuation: the market value of the REIT holdings, a income multiple on stabilized income assets & the asset management business, and book values on the development assets.

The “Bear” Case:

REIT Holdings Value: $310M

Today, the REIT values to Dream are about $400M in straight up market value, comprised of 29% ownership in the Office REIT and 24% ownership in the Alternatives REIT. Backing the market value of the REITs out of the $870M market cap of DRM means the DRM equity is really valued at about $470M currently. I got to the $310M number above by assuming the both REITs’ market caps fall (further than they already have) to about half of their current book value. In normal times the REITs seem to trade around book, but currently the Office REIT trades at about 70% of book and the Alternatives REIT trades at 60% of book. Both were hit fairly hard in the early days of the COVID crisis and have recovered little. My base case is that in the next few years real estate values revert back to roughly their pre-COVID levels, but assuming that the value of their assets gets cut in half seems pretty conservative to me. Note here that I am completely ignoring the value of the distributions from the REITs themselves which totaled about $20M in 2019.

Income Producing Assets Value: $80M

Normalized annual net margin on these assets looks to be about $15M (again, with intent to grow in the future). Standalone public companies in the “real estate operating companies” sub-industry trade around 10x TTM P/E currently. I’ve assumed the “E” here declines by about 20% and you get further P/E ratio compression of 1/3rd (i.e. $12M annual income x 6.6 P/E = $80M). I think you could validly poke holes in either of these assumptions. The mix of assets is pretty diverse but does include office properties and a major recreational property (the ski hill) that could see real impairment. You could also argue the multiple one way or another – perhaps it’s way too high unless this were a standalone entity, perhaps it’s way too low even in today’s uncertain environment. The idea here is to be conservative and I think this get us there.

Asset Management Business Value: $45M*

The management and development fees from the asset management business generate about $10M in annual net margin. Public companies in the general “asset manager” space average about 13x TTM P/E. I get to $45M by assuming the fees are cut in half (as the value of the public REIT assets fall drastically) and that multiples compress by 1/3rd (i.e. $5M x 8.5 P/E = ~$45M). The management fees themselves seem typical for most REIT managers: some percentage of net assets (subject to a hurdle rate) with other function specific fees sprinkled in. The development fees tend to be lumpier as they are one-time fees based on specific projects within the partnerships/REITs. I think it would be very difficult to model the revenues streams with any real accuracy, so I’m assuming that getting cut in half would be conservative enough here. I would also point out this cohort of asset managers is not real estate specific – it is asset managers in general (i.e. mutual fund families, companies with broker/dealer or private wealth management businesses, etc.) – so the comparison is not apples to apples. You could make the argument that this multiple should be higher for a real-estate focused manager, or lower because the business would be so small as a stand alone entity, or any direction you want really. Again, I’m just trying to get in the ballpark here.

Development Assets & Corporate-Level Value: $100M

One nice thing Dream does in the financials is break down all of their statements by segment. I walked through all of the individual “recurring income” lines of business above, but for the rest of the value I am lumping together the development segment and the other corporate-level assets & liabilities. The corporate “equity” is accounted for separate from the recurring income or development segments and mostly consists of cash/debt that is not specific to any particular project. FYI, one unfortunate change in the most recent quarter’s financials was the way Dream discloses the balance sheet assets/liabilities for the segments so I am basing this piece of the valuation on the year end 2019 financials rather than the most recent quarter’s balance sheet.

I arrived at the $100M above by first applying a 50% discount to the development segment’s land, housing, condo, and investment property inventories as well as any capital/other operating assets (i.e. anything that might be actual property they own). Then, I add in all of the other assets and back out all of the liabilities from the development segment and the corporate-level holdco to get to the book value of $100M.

My point here with the 50% discount is to allow for the fact that maybe Dream made colossal mistakes in purchasing the properties they did and will do nothing in the future to improve the value of those assets (i.e. they will not actually develop them). My concern here is: Dream’s newer assets have increasingly been located in the Toronto and Ottawa markets which have seen substantial growth and appreciation in the last few years and could perhaps see a reversion in values. Alternatively, Dream has a ton of legacy assets (namely 9,000 acres of land) in less “sexy” West Canada markets like Calgary, Saskatoon, Edmonton, and Regina where slacking oil/commodity prices are impacting the local markets. Development assets are held on the balance sheet at the lower of cost or net realizable value, so in reality I’d bet that the fair value of these assets in aggregate is greater than book value, but lets just assume Dream paid 2x what they should have and still owe on the associated debt/liabilities. You still get $100M in book value in a cataclysmic scenario like that.

Total “Bear” Case Equity Value: $535M (-38% from current market value)*

The “Reasonable” Case:

REIT Holdings Value: $480M

The $480M value assumes that the REITs close 1/2 of the gap between their current P/B and full book value (for example, the Office REIT goes from 70% of book to 85% of book). It’s not rocket science, but I feel that this reasonably allows for some impairment on the assets and/or continued short term disruptions in collections. This also ignores the upside of the REITs recovering to their full book value (which would be $585M in equity value for Dream).

Income Producing Assets: $120M

Here, I just assumed the full 10x multiple (cited above) on $15M in TTM net margin. I still think this is relatively conservative given quality of the underlying assets. This valuation also gives little optimism for future growth in the income stream, which management has specifically prioritized.

Asset Management Business: $100M*

For the asset management business, I assumed a modest 10x multiple on TTM net margin. I think this is relatively conservative but justified given the current state of things. Dream manages about $9B in assets, which strikes me as fairly small in the global real estate world. The majority of their experience has been within their own public vehicles (DRM and the REITs) with some smaller private partnerships. That being said, Dream recently announced a new private investment division (Dream Equity Partners) as the newest extension of the asset management business. If DRM could get some traction with allocators over the next few years, I see this as a potential engine for growth.

Development Assets & Corporate-Level: $650M

This is just the book value of the development and corporate-level assets/liabilities. I’ll be honest I still have no idea how to handicap the value of the development assets. On one hand there are the dangers I discussed above: perhaps the hot Toronto market that Dream has increased their exposure to cools off and the Western Canada assets continue to decline in value. On the other hand, if things do normalize or even continue to appreciate, the book values are probably understating even the current value of the assets, much less the future value of the fully developed assets. I think this is probably the biggest question mark for me, but I’m putting my faith in Dream’s successful track record here and trusting in the strategy. I think there’s a good chance this is a very conservative value for this piece of the business.

Total “Reasonable” Case Equity Value: $1,350M (+55% from current market value)*

So in summation, I think you are looking at a relatively attractive risk profile given a pretty apocalyptic “bear” scenario and a “return to normal” scenario. To be honest, I believe that the “reasonable” scenario outlined above still leaves a lot of potential value unaccounted for, but I try to be more thoughtful about my downside than my upside. Consequently, $1.4B is roughly book value for DRM, which the market has shown a willingness to value DRM at as recently as Q4 2019.

The Bad:

If you can’t tell already, probably the thing I worry the most about is Dream’s Toronto exposure. When it comes down to it, I have no real idea whether Toronto property has been irrationally bid up in the past few years or is on a sustainable long term trend given its growing global profile. I’ve seen all the anecdotes about foreigners speculating on core “greater Toronto area” (GTA) commercial and residential RE in hopes of unloading it to some greater fool in the future and COVID will undoubtedly force corporates and residents alike to re-assess the need for expensive metro property going forward. So it’s possible that Toronto (and to a lesser extent Ottawa) are not the no-brainer bet they have been in the recent past, but Dream has obviously decided this is where their future is, so they’ve pivoted hard in that direction while unloading legacy western Canada assets. Ultimately, I don’t know what the future looks like but my base case is that COVID put a small pause on a macro growth trend in eastern Canada that will continue into the future. If that is the case I think Dream reaps the rewards.

Heavy insider ownership cuts both ways. It can be a great alignment of incentives but it also means certain insiders wield nearly total control. I think that you have to be comfortable with who’s in charge here and President Michael Cooper seems as capable as anyone. Cooper holds 40% of the economic interest and nearly all of the voting power in the company and under his tutelage Dream has put together a strong track record of creating value. I have no reason to expect that to be any different moving forward, but it still feels like a lot of the success or failure of DRM will be tied to Cooper’s decision making. It does make me a little nervous, but it’s something I think I can live with. Here are a couple pieces to give you a feelforCooper.

One of the other downsides I think about with Dream is that there’s this “conglomerate” discount that gets applied to the stock. It’s a mix of businesses that are traditionally siloed off from one another. It’s part REIT, part developer, and part asset manger. My perception is that this mix of business lines plus all of the legacy exposure to western Canada weighs on the market multiple here. I don’t know that there’s an obvious way for them to overcome that , but that’s also a big component to why I think there’s an opportunity here. The market will simply have to come around to realizing the value at some point.

The Key Variables:

The key things I am looking for from Dream are:

Short-term collections and write-down trends: I plan on keeping an eye on these because I think they will give some indication of the intermediate term impact of COVID. Of particular interest will be DRM’s reactions to these trends as I think that will tell us how worried they are about their existing asset portfolio.

Asset management growth: continued traction in the asset management line of business would help create more diversified revenues and potential for more exponential growth. Demonstrated market interest in the new Dream Equity Partners division would be exciting to see.

Leverage: although Dream seems conservatively positioned to me, especially against peers, leverage is very much part of the development playbook and inherently makes me nervous. I will probably keep a closer eye than most on the debt levels moving forward.

Conclusion:

So, I hope by this point I’ve made clear that I think there is a lot of value here with Dream. It’s more than a traditional real estate business and has some built in optionality that I think makes for an attractive opportunity. Also, I think the quality of the underlying assets and the management create limited downside for the business. I’ve mentally categorized this as one of my deep value/mean reversion holdings and put the position in at about a 7% position in late May.

Sawbuckd

*Edit: I goofed! In the initial version of this post, I incorrectly estimated that earnings from the asset management business was roughly $25M/year (excluding development fees). This figure did not properly account for the loss of revenues previously collected from the Global REIT (which was sold to Blackstone in 2019 and therefore will not be contributing to revenues moving forward). The $10M reflected above is a more accurate representation of management and development fees moving forward. My previous “bear” and “reasonable” valuations for the AM business was $110M & $200M, respectively. This translated into original “bear” and “reasonable” valuations for DRM at $600M & $1.5B, respectively. Oops! Special thanks to Tyler from Canadian Value Stocks for showing me the error of my ways.

In previous posts I’ve alluded to some of the merger arbitrage situations that I’ve dipped my toe into and I thought it was time I wrote them up. These write ups are more brief than my other long ideas, but I hope that you find them helpful.

I want to point out a couple of things before we get started:

I am still relatively new in the world of “special situations.” You should always do your own homework (especially when it comes to stock tips from anonymous twitter accounts), but you should definitely always do your homework when the author says “I’m still getting the hang of this” – so consider yourself warned.

In general, I only put positions into the portfolio that I can reasonably expect to achieve a 15% CAGR. Standard merger arbitrage deals have very low spreads that typically cannot hit this level of return. I expect there is a reasonable probability that the deals described below hit my hurdle or higher, therefore you should reason that these positions are very speculative (especially relative to other mergers). The downside on these could be -50% or more if the deal busts. Given this and point 1 listed above, I size these positions accordingly – they are very very small for me.

I only consider all cash deals, so no shorting here.

My DD process is to review the deal document, do some basic research on the involved parties, review any relevant news/analysis, and take my best guess at the outcome. This is NOT a bullet proof vetting process involving channel checks, expert networks, or sophisticated modeling. I completely own up to the fact that I could be missing something big and obvious in any of these situations and could be lighting money on fire.

*If you only read one of these, skip down and read the CETV write up at the bottom!*

Without further ado:

Wright Medical Group (WMGI)

Deal Price: $30.75 Deal Close Target: 2H 2020 Sawbuckd Basis: $27.50 (~12% spread, 04/30/20) Current Price: $29.28 (~5% spread, as of 06/25/20)

In November of last year, medtech behemoth Stryker (SYK) announced they were acquiring medical device developer Wright Medical Group (WMGI) in a $5B deal at $30.75/share in cash with a scheduled close of 2H 2020. Stryker has a strong balance sheet and ample access to capital to close the deal (they recently issued a few billion in debt carrying yields 1.15% to 3% and maturities ranging from 5 to 30 years). So, I have little doubt of SYK’s ability to close and they’ve shown no signs of buyer’s remorse thus far. I think the deal makes strategic sense as WMGI adds a unique product portfolio to SYK’s already massive array of offerings and had a number of serious suitors in addition to SYK. The risk here is a mix of “regulatory” (WMGI is based in Amsterdam and both companies operate globally so there will be a number of regulators involved) and “timing” (could take longer than anticipated to get the necessary approvals), but neither strike me as particularly worrisome. In my opinion, the point at which I got in (12% spread) was more a function of spreads having blown out on almost every arbitrage deal across the market in the wake of COVID rather than a true reflection of the real risk in the deal. So let’s consider the downside here: assuming we apply a pessimistic 20% discount to the $20.50 pre-deal/pre-COVID trading price a broken deal here still implies just a 75-80% chance of the deal completing – which felt too low to me back in late April. All that said, while I think that risk/reward scenario was pretty attractive at the time, today’s 5% spread would not be something that interests me.

FitBit (FIT)

Deal Price: $7.35 Deal Close Target: Q4 2020 Sawbuckd Basis: $6.34 (16%, 05/29/20) Current Price: $6.35 (16%, 06/26/20)

Towards the end of 2019, Google announced that it was acquiring the well-known wearable tech company Fitbit in a $2B deal valuing FIT shares at $7.35 with a targeted close date of November 2020. Declining sales and mounting losses over the last few years had made it clear that FIT was losing the battle to Apple watches and other more popular wearables. Candidly, this seems like the optimal outcome for everyone involved at this point: the transaction is a rounding error for Google but gives them additional user data to leverage within the larger Googleplex while simultaneously giving a quiet and dignified end to Fitbit as a standalone public entity. I have no doubt about Google’s ability or willingness to close this deal – the primary risk factor here is that regulators drop the axe. It seems that anything Google does now draws the ire of watchdogs and regulators alike, but Google’s messaging has been on point since the initial announcement when they stated that they will not use Fitbit’s user data in conjunction with Google Ads. While Google’s recent (and increasingly frequent) conflicts with regulators are keeping this spread pretty wide, I am betting on status quo this time around. Google has closed hundreds of acquisitions in its history and pays tens of millions in lobbying expenses across the globe each year – my bet here is that they get this one done despite the privacy and antitrust concerns. The downside is pretty ugly here: pre-deal and pre-COVID FIT was at $3.15. Despite a $250M break fee in the event of a regulatory block, I’m assuming the bottom here is still probably -50% against the 16% upside which would make the implied probability of closing the deal about 75%. We get more clarity soon as the European Commission will be ruling on the deal 07/15/20 and the Australian Competitive and Consumer Commission (ACCC) will be ruling 08/13/20. Buyer beware I think this is a pretty hairy situation – do your own homework.

CETV is a media and entertainment company broadcasting 30 television channels to over 45 million viewers across five Central and Eastern European markets (Bulgaria, the Czech Republic, Romania, the Slovak Republic and Slovenia). In October of 2019, CETV announced that their majority shareholder, AT&T (T), had agreed to sell the company to PPF Group – a privately owned conglomerate of various global businesses – in a $2B all cash transaction valuing CETV shares at $4.58/share. This is quietly one of the most bizarre and fascinating acquisitions I have looked at. First, PPF is the personal investment vehicle for the Czech Republic’s richest man, Petr Kellner, who amassed his fortune by capitalizing on the privatization of old Czechoslovakian assets in the early 90s following the fall of communism across the defunct Eastern Bloc. Second, Kellner/PPF’s motives for acquiring CETV have been called into question – mostly because of Kellner’s connections to China and his alleged attempt to launch a domestic “propaganda campaign” on China’s behalf in the Czech Republic. Third, based on all this weird China stuff, U.S. Senator Marco Rubio stuck his nose into the situation by asking the Trump administration to look into the acquisition while citing the PFF/China connection as matter of national security. [Also, somewhat unrelated to the acquisition, one of CETV’s stations was defrauded out of $75M by a man who was also responsible for the murder of Slovak journalist who’s death indirectly caused the resignation of the Prime Minister of Slovakia.] So, to say there’s some controversy around this deal is probably an understatement.

Ignoring all of this and re-focusing on the deal fundamentals, CETV has spent the last few years improving their operations and paying down a mountain of debt to a more reasonable level. Share price responded nicely and had been on a solid run over the 12 months preceding the deal announcement. To that end, shares actually traded above the deal price (at a seemingly reasonable 15-18x TTM P/E) in the 4-5 months prior to the announcement. It’s odd that the deal price had no premium built in, but I would bet AT&T was not a tough negotiator as this was a legacy holding brought over in the Time Warner merger and they are already being pressured to pair down their non-core businesses. Given all of that, I will take a shot in the dark on the downside here. If you assume it’s 50/50 probability the deal goes through, your downside would have to be $2.15/share (-36% downside) to break even. That’s an implied TTM P/E of 7 which seem pretty cheap to me. In the short term, assuming a deal break, I suppose there could be a wave of initial selling from arbs, but then again I don’t really know if there are many arb shops in this deal given the level of uncertainty/controversy. Regarding the willingness/ability for PPF to close, beyond being backed by the richest man in the Czech Republic, I’d say I would prefer they actually be a secret pawn of China – at least then their funding would be completely secure and there would be some compelling political motives to ensure the deal went through. CETV has communicated a Q3 2020 expected close for the transaction, which means this could be a whopper if it does close on time. Given the size of this spread, I feel a bit like a patsy at the poker table here, but given what I see this seems like a very hairy but potentially compelling opportunity. I would love to hear from anyone who’s more informed on the matter.

Collector’s Universe is a niche business with extremely attractive economics and a path to moderate growth.

A solid balance sheet and asset light business model create limited downside expsosure.

Buyer Beware: I am a little tardy on this write up and the shares have run since I put in my initial position back in March- at current prices I would not be buying.

The Numbers (as of 6/10/20):

Current Price: $26.47/share

Sawbuckd Basis: $18.56/share

Mkt Cap: $245M

EV: $237M

EV/EBITDA (LTM): 11x